Basic Accounting for New Entrepreneurs

Running a small business can be an exhilarating experience, but it's not without its challenges. From managing staff to dealing with suppliers and customers, there are always countless tasks vying for your attention. However, one task that's often overlooked, but is absolutely vital, is accounting.

Yes, we know, accounting might not be the most exciting topic in the world, but it's one that could make or break your business. After all, if you're not keeping a close eye on your finances, how do you know if your business is profitable, or if you're spending too much money in one area? As the saying goes, a penny saved is a penny earned.

Now, you might be thinking that you'll just hire a bookkeeper or accountant to handle all this for you, and that's great. However, it's still important for you to know the basics of accounting. This will help you stay on top of your business's finances, and ensure that you're making informed decisions.

Don't worry, you don't need to be a maths genius to understand accounting. It's all about keeping track of your income and expenses, and making sure that you're paying the right amount of tax. With a little bit of practice, you'll soon get the hang of it.

History

Accounting has been practised for centuries, but modern accounting can be traced back to Luca Pacioli's book on double-entry accounting in the late 15th century. Accounting has evolved over time to adapt to changing business needs and technological advancements, such as the development of complex accounting systems during the industrial revolution and the use of computers in the 20th century. In the present day, accounting is essential for small business owners to effectively manage their finances, track income and expenses, and make informed decisions.

Essential Accounting Terms and Concepts Every Business Owner Should Understand

In order to understand accounting for small businesses, there are several key concepts and principles that are important to know such as:

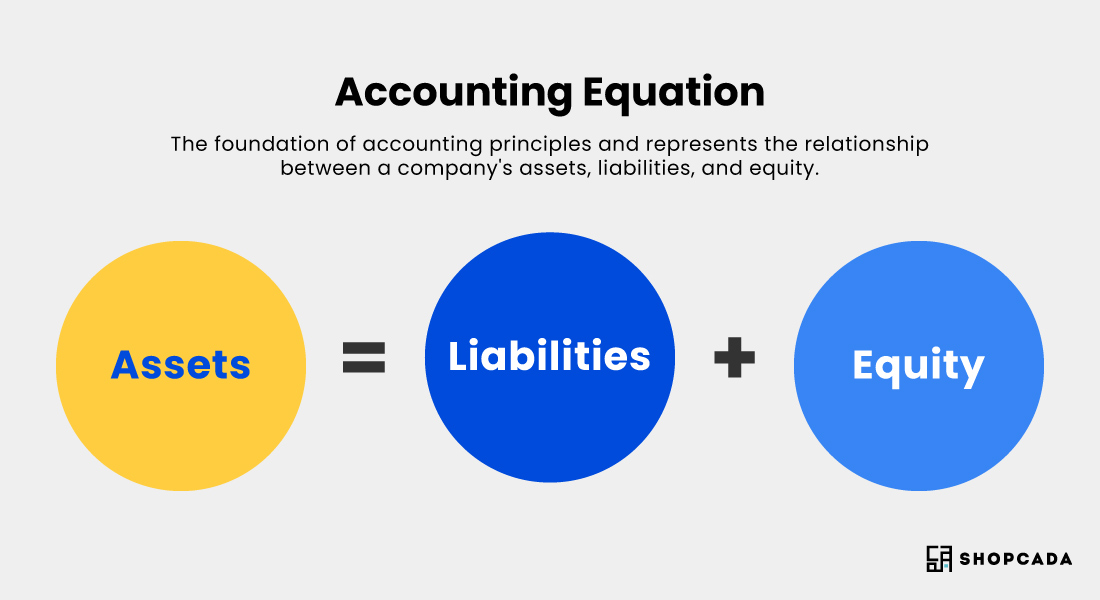

Accounting Equation

The accounting equation is the foundation of accounting principles and represents the relationship between a company's assets, liabilities, and equity. It is expressed as follows:

Assets are the resources owned by a company that have a monetary value and can be converted into cash, such as cash, accounts receivable, inventory, and equipment.

Liabilities are obligations that a company owes to others, such as loans, accounts payable, and taxes.

Equity represents the value of a company's assets after all liabilities are paid off. It is the residual interest in the assets of the company after all debts and obligations are accounted for, and it is owned by the company's shareholders.

The accounting equation must always balance, meaning that the total value of a company's assets must equal the sum of its liabilities and equity. This ensures that a company's financial statements accurately reflect its financial position and provides a basis for making informed decisions about the business.

By understanding and applying the accounting equation, business owners can keep track of their financial transactions, accurately record their business activities, and make informed decisions to manage their finances and grow their business.

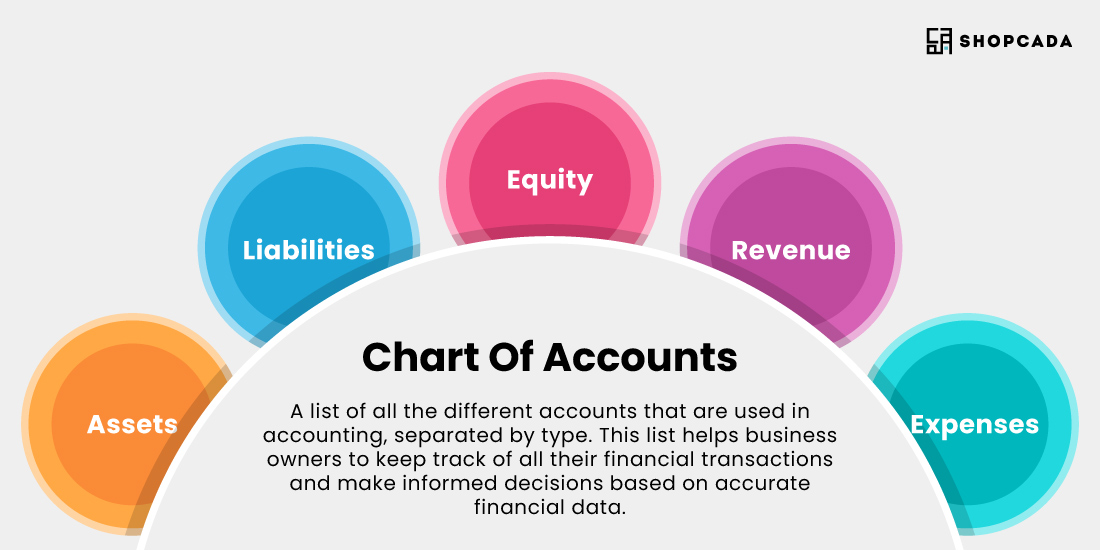

Chart Of Accounts

The chart of accounts is a list of all the different accounts that are used in accounting, separated by type. This list helps business owners to keep track of all their financial transactions and make informed decisions based on accurate financial data.

In general, the chart of accounts will include five main types of accounts: assets, liabilities, equity, revenue, and expenses.

Each account in the chart of accounts is assigned a unique number or code. This makes it easier to organise and sort the accounts, especially when there are many of them.For example, assets might be assigned numbers in the 100s, liabilities in the 200s, equity in the 300s, revenue in the 400s, and expenses in the 500s. Within each of these categories, accounts can be further broken down into subcategories.

For instance, under assets, you might have subcategories such as current assets (such as cash and accounts receivable) and fixed assets (such as property, plant, and equipment). This allows for even greater organisation and specificity in tracking financial data.

The chart of accounts is a comprehensive list of all the accounts that a business uses to record its financial transactions. It is an essential tool for organising and tracking financial data, ensuring accuracy and consistency in accounting practices, and enabling efficient financial reporting.

A well-organised and properly maintained chart of accounts can help business owners to make informed financial decisions, identify areas of financial strength or weakness, and monitor the performance of their business over time. It also enables business owners to meet their legal and regulatory obligations, such as tax reporting and compliance with financial reporting standards. Therefore, it is crucial for small business owners to take the time to set up and maintain a suitable chart of accounts for their business.

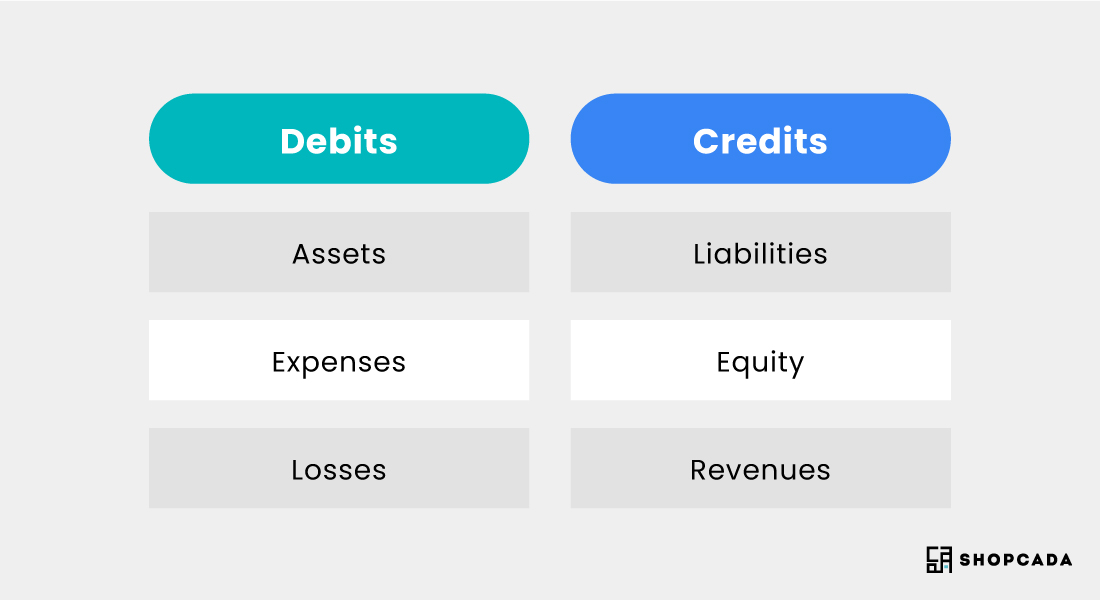

Double-Entry Bookkeeping

Double-entry bookkeeping is a system of accounting where every financial transaction a company makes is recorded in two accounts. This system ensures that every transaction is accurately recorded and that the financial statements are accurate.

For every transaction, two entries are made: a debit and a credit entry. A debit is an entry made to the left side of an account and increases assets and expenses, while a credit is an entry made to the right side of an account and increases liabilities and equity.

Common debits and credits that new business owners should know

Debits

Debit is a fundamental concept in accounting that refers to the recording of an entry in the left-hand side of a ledger or account. In accounting, every financial transaction involves at least two accounts - a debit account and a credit account.

In simpler terms, a debit can be thought of as money coming into the account or an increase in value of an asset. It is important to note that a debit in one account must always be offset by an equal and opposite credit in another account, ensuring that the overall accounting equation remains balanced.

Assets

Assets are the resources owned by the business, such as cash, accounts receivable, inventory, and equipment. When an asset increases, it is recorded as a debit entry, and when it decreases, it is recorded as a credit entry. For example, if a business receives cash from a customer, the cash account would be debited, and the accounts receivable account would be credited.

Expenses

Expenses are the costs incurred by the business in order to generate revenue, such as rent, salaries, or utilities. When an expense is incurred, it is recorded as a debit entry, and when it is paid, it is recorded as a credit entry. For example, if a business pays rent for its office space, the rent expense account would be debited, and the cash account would be credited.

Losses

Losses are decreases in equity resulting from transactions that are not related to the normal operations of the business, such as a loss from a lawsuit or a natural disaster. When a loss occurs, it is recorded as a debit entry, and when it is recovered, it is recorded as a credit entry.

Credits

In accounting, credit is a crucial concept that refers to recording a financial transaction on the right-hand side of a ledger or account. Every transaction involves two accounts: a debit account and a credit account.

Simply put, credit represents money leaving the account or a reduction in the value of an asset. It's essential to remember that a credit entry in one account must always be balanced out by an equal and opposite debit entry in another account. This ensures that the accounting equation remains balanced and accurate.

Liabilities

Liabilities are the obligations of the business, such as accounts payable, loans, or taxes payable. When a liability increases, it is recorded as a credit entry, and when it decreases, it is recorded as a debit entry. For example, if a business takes out a loan, the loan payable account would be credited, and the cash account would be debited.

Equity

Equity represents the owner's investment in the business and the retained earnings of the business. When equity increases, it is recorded as a credit entry, and when it decreases, it is recorded as a debit entry. For example, if a business owner invests money into the business, the equity account would be credited, and the cash account would be debited.

Revenues

Revenues are the amounts earned by the business from the sale of goods or services. When revenue is earned, it is recorded as a credit entry, and when it is received, it is recorded as a debit entry. For example, if a business sells a product to a customer on credit, the accounts receivable account would be credited, and the revenue account would be debited.

It's important to understand the principles of debits and credits in order to maintain accurate financial records for your business. By keeping track of your debits and credits, you can ensure that your financial statements are accurate and comply with accounting standards. It's also important to consult with an accountant or bookkeeper to ensure that your financial records are accurate and up-to-date.

Financial Reports Every Small Business Owner Should Know

As new entrepreneurs, it is important to keep track of your financial records to make informed business decisions. There are several key financial reports that can help you understand the financial health of your business. Here are some of the most important financial reports that every small business owner should know:

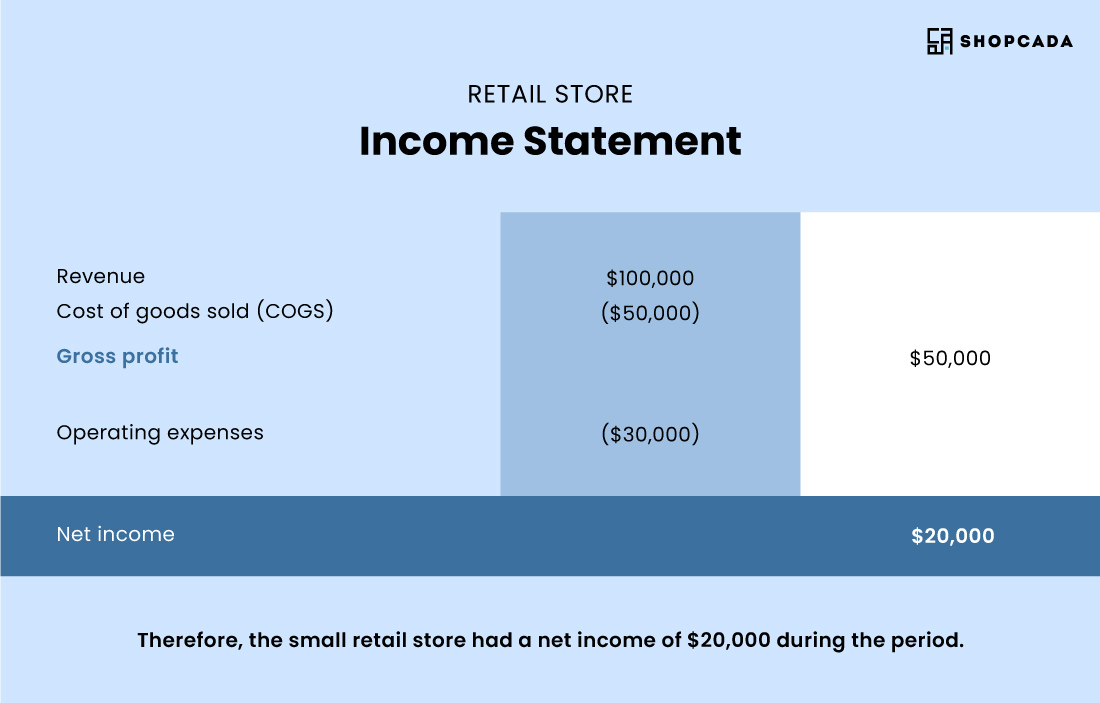

Income Statement (Profit & Loss Statement)

The income statement, also known as the profit and loss statement (P&L), is a report that shows the revenues, expenses, and net income or loss of a business for a specific period. It's one of the most important financial reports that a small business owner needs to understand because it shows whether the business is profitable or not.

The income statement has four main components: revenue, cost of goods sold (COGS), gross profit, and expenses. The revenue is the money that the business earns from its sales or services. COGS is the direct cost associated with producing or delivering the goods or services sold. Gross profit is the difference between the revenue and COGS. Expenses are the indirect costs of running the business, such as rent, utilities, salaries, and marketing. The net income is the result of subtracting the expenses from the gross profit.

Example: A small retail store generates $100,000 in revenue and incurs $50,000 in COGS, resulting in a gross profit of $50,000. The store then spends $30,000 on expenses, such as rent, salaries, and advertising, resulting in a net income of $20,000 for the period.

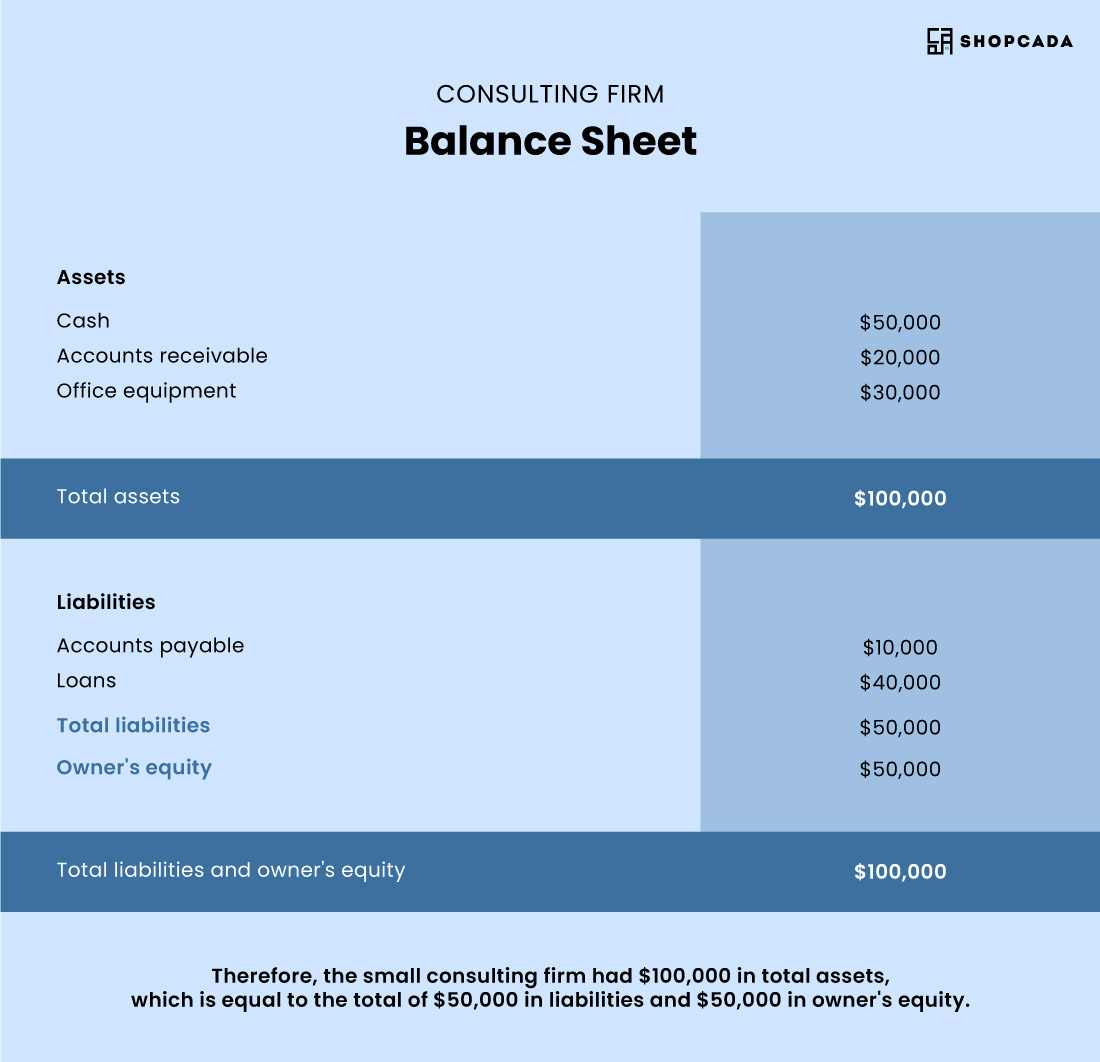

Balance Sheet

The balance sheet is a report that shows the financial position of a business at a specific point in time. It lists the assets, liabilities, and owner's equity of the business, and the total assets must always equal the total liabilities plus owner's equity. The balance sheet is essential for small business owners because it helps them understand the liquidity of their business, which is the ability to pay bills and debts when they are due.

Assets are the resources owned by the business, such as cash, inventory, equipment, and accounts receivable. Liabilities are the obligations of the business, such as loans, accounts payable, and taxes. Owner's equity represents the investment made by the owner into the business, plus the accumulated profits or losses.

Example: A small consulting firm has $50,000 in cash, $20,000 in accounts receivable, and $30,000 in office equipment, totaling $100,000 in assets. The firm also has $10,000 in accounts payable and $40,000 in loans, totaling $50,000 in liabilities. The owner's equity is $50,000, resulting in a total of $100,000 in assets, which equals the total of $50,000 in liabilities plus owner's equity.

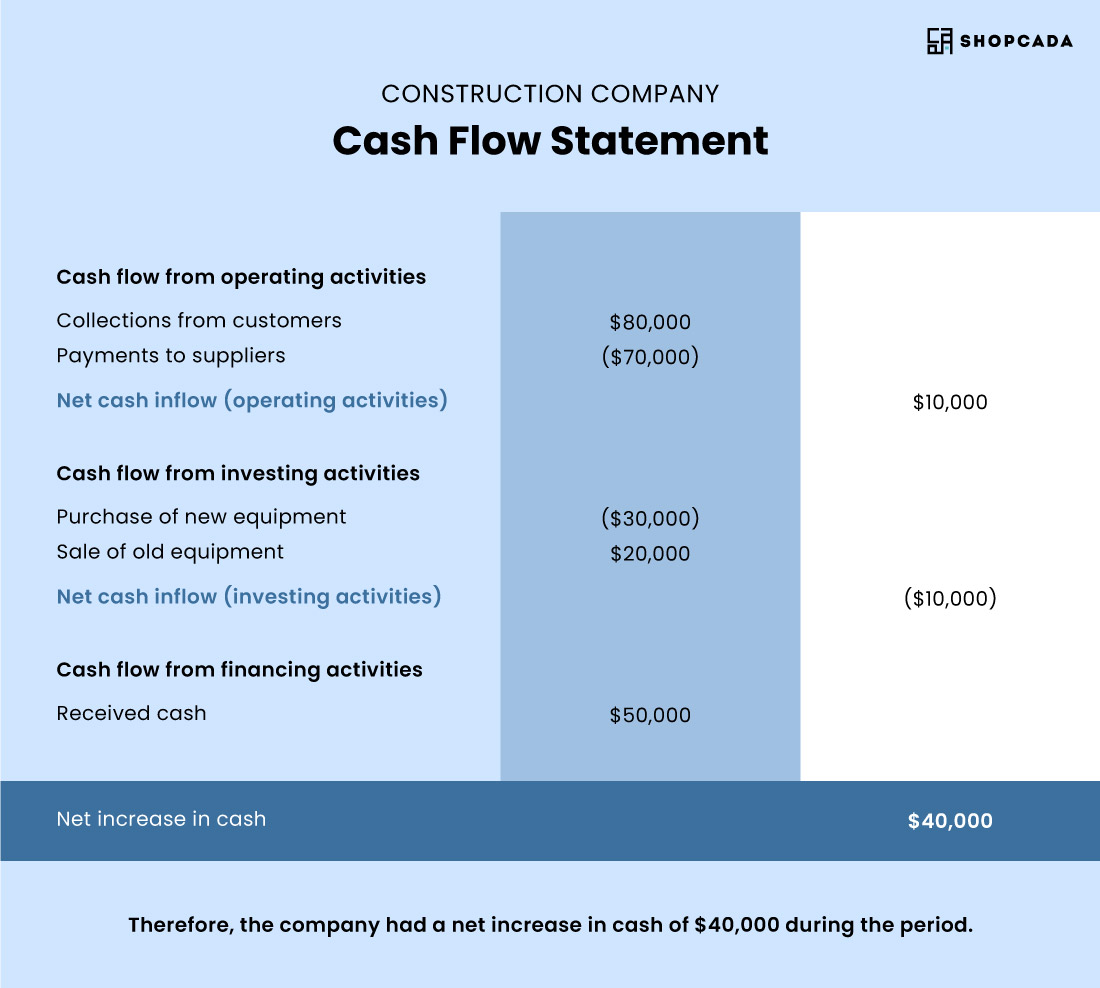

Cash Flow Statement

The cash flow statement is a report that shows the inflows and outflows of cash in a business for a specific period. It's crucial for small business owners because it helps them understand the cash position of their business, which is different from the profit position. The cash flow statement has three main components: operating activities, investing activities, and financing activities.

Operating activities are the cash flows generated from the business's normal operations, such as sales, collections from customers, and payments to suppliers. Investing activities are the cash flows generated from buying or selling long-term assets, such as equipment or property. Financing activities are the cash flows generated from financing the business, such as loans or investments.

Example: A small construction company has $100,000 in sales, $80,000 in collections from customers, and $70,000 in payments to suppliers, resulting in a net cash inflow of $10,000 from operating activities. The company also spends $30,000 on new equipment and receives $20,000 from selling old equipment, resulting in a net cash outflow of $10,000 from investing activities. The company receives $50,000 which results in the company gaining $40,000 in that period.

Accounts Receivable Ageing Report

The accounts receivable ageing report shows how much money your customers owe you and for how long. It helps you keep track of unpaid invoices and helps you identify which customers are slow to pay.

For example, a small business owner who provides consulting services can use the accounts receivable ageing report to identify which clients have overdue invoices and follow up with them for payment.

Budget vs. Actual Report

The budget vs. actual report compares your actual financial results to your budgeted expectations. It helps you identify areas where you exceeded or fell short of your goals and helps you adjust your future plans accordingly.

For example, a small business owner who owns a fitness studio can use the budget vs. actual report to determine if they spent more than anticipated on advertising and adjust their future advertising budget accordingly.

By regularly reviewing these key financial reports, small business owners can make informed decisions about their business operations and finances, identify potential problems early on, and take steps to address them.

Apps That Can Help New Entrepreneurs with Bookkeeping

Here are 5 apps that can help new entrepreneurs with bookkeeping without requiring the services of an accountant:

QuickBooks Self-Employed

This app is designed for self-employed individuals and freelancers. It allows users to track expenses, send invoices, and estimate quarterly taxes. QuickBooks Self-Employed also integrates with popular payment systems like PayPal and Square.

FreshBooks

FreshBooks is an accounting software that is designed to be user-friendly for small business owners. It features time tracking, invoicing, and expense tracking. FreshBooks also has an app that allows users to access their financial records from their mobile devices.

Wave

Wave is a free accounting software that offers invoicing, expense tracking, and receipt scanning. It also offers the ability to accept payments from customers and integrates with popular payment systems like PayPal and Stripe.

Expensify

Expensify simplifies expense reporting by allowing users to scan receipts and track expenses on the go. It also allows for easy reimbursement for employees and offers features for managing business travel expenses.

Xero

Xero is an accounting software that offers features like invoicing, expense tracking, and bank reconciliation. It also integrates with more than 800 third-party apps, such as PayPal and Square, making it a versatile tool for managing business finances.

Using these apps, new entrepreneurs can manage their finances effectively and easily without the need for an accountant. They can save time and money while still having access to the tools they need to manage their finances.

Closing Words

Basic accounting for small business owners is an essential skill that can help ensure the success and longevity of their business. By understanding the accounting equation, double-entry bookkeeping, and the chart of accounts, business owners can accurately track their financial transactions and make informed decisions for their company.

It is also important for small business owners to maintain accurate and up-to-date financial records. This can be achieved through the use of accounting software or hiring a professional accountant. By keeping track of their financial transactions and regularly reviewing their financial reports, business owners can gain insight into the financial health of their business and make informed decisions about its future.

In addition to these practical aspects of accounting, there are also ethical considerations to keep in mind. Small business owners should strive to maintain honesty and transparency in their financial practices, avoiding fraudulent or misleading activities that could harm their business or stakeholders.

Overall, basic accounting for small business owners is a crucial skill that can help ensure the success and longevity of their business. By understanding the foundational principles of accounting, maintaining accurate financial records, and making informed decisions based on financial reports, business owners can achieve their goals and grow their business in a sustainable and ethical manner.